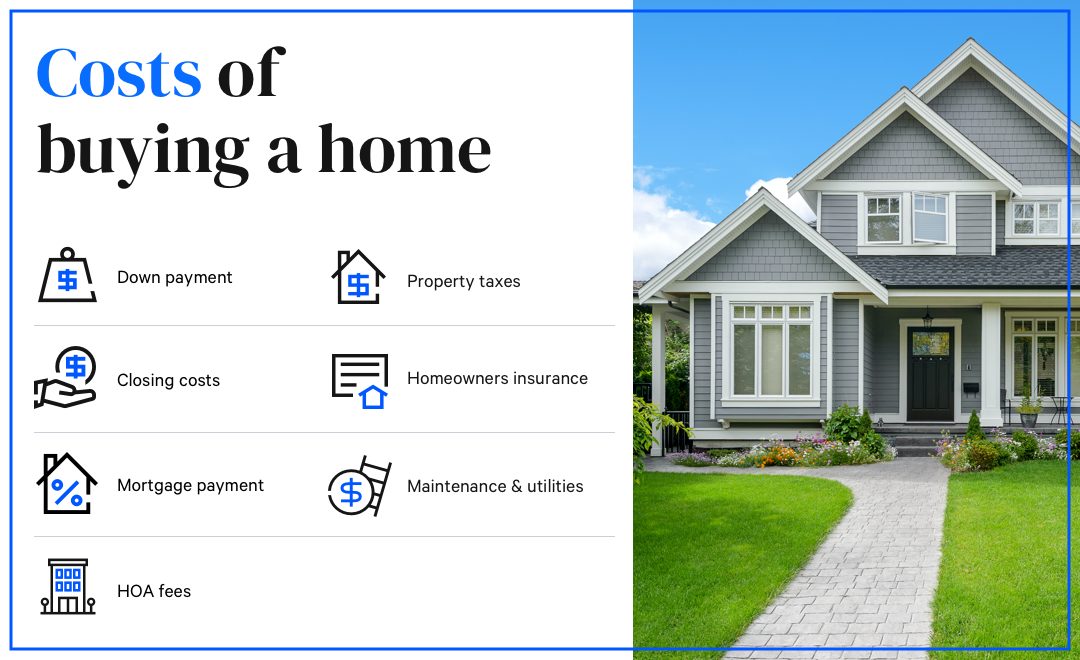

Be Ready for the Additional Costs of Buying a Home

While there are a lot of great surprises in life—unexpected birthday parties, a scratch-off ticket win, or meeting the love of your life on the internet—there are also plenty of not-so-pleasant surprises that may come your way. If you’re lucky enough to be tipped off about some of them, you can avoid running headlong into trouble. When buying a home, plenty of buyers—especially first-time buyers—are caught unaware by the additional expenses involved. These “hidden costs” can add up quickly, putting you in a less-than-ideal position.

At Ernest Homes, we want to make sure you have all the information you need to make an informed decision about homeownership. If your goal is to own new construction in Savannah, GA or one of its surrounding communities, read on. We’re here to give you a heads-up on some little-known facts about the financial side of buying a new home.

Fees – What You Can Expect

- Government recording charges: State and local governments charge fees to record your deed, mortgage, and loan documents.

- Appraisal fee: A licensed appraiser will determine how much your home is worth, and you’ll pay this cost.

- Credit report fees: You’ll cover the cost of the credit reports your lender ordered.

- Title services and lender’s title insurance: These fees are associated with researching and securing your home’s title.

- Flood life-of-loan fee: This fee covers monitoring of your property’s flood zone status.

- Tax service fee: Ensures previously paid property taxes are accurate and current.

- Lender’s origination fee: This covers the cost of processing your loan application.

- Attorney’s fees

You can't eliminate all fees, but some can be waived or negotiated. Application fees—often $100 or more—are a good place to start. If you compare lenders, you may find one with lower closing costs; just be sure to compare loan terms carefully.

Inspections and Surveys

Some purchases may require home inspections or land surveys to “close the deal,” especially if your lender requests them.

Taxes, Taxes, Taxes

Property taxes are part of homeownership, but many buyers forget a portion is due at closing. Escrow accounts—used by lenders to pay taxes, homeowner’s insurance, and HOA dues—are typically required if your down payment is less than 20%. When you close, expect to pay:

- A few months’ worth of property taxes

- A full year of homeowner’s insurance

- HOA dues, if applicable

Moving Expenses Can Add Up

Will you need movers, rental trucks, hotel stays, or airline tickets? Will you need to buy new furniture or replace items that are too bulky to transport? Factor these costs into your budget early.

Utilities

Utility companies may charge setup fees or require deposits. If you’re moving to a larger home, expect higher heating, cooling, and water bills, along with possible new service fees such as trash collection.

Insurance – Above and Beyond

All mortgages require homeowner’s insurance. But you may need additional coverage depending on your down payment and location:

- Private Mortgage Insurance (PMI): Required if you put down less than 20%. PMI protects the lender if you default. Learn more here.

- Hazard and catastrophe insurance: Depending on your region, you may need extra coverage for floods, windstorms, tornadoes, or earthquakes.

Most homeowners can drop PMI once they owe less than 78% of the home’s original value—check with your lender for exact requirements.

Now that you’re aware of some unexpected costs you may face when buying a home, you’ll be better prepared for your purchase process. If you still have questions, don’t hesitate to call our team at 912-660-9673 or send us an email. We’re always happy to help you estimate the full costs of homeownership.